Emerging Markets Haven't Hit Bottom Yet

September 26, 2015

When Mark Mobius urges caution on emerging markets, you know they’re in trouble. The septuagenarian executive chairman of Franklin Templeton’s emerging-markets group has been boosting the asset class for decades, exhorting investors to pile back in after crises and meltdowns. Now, not so much. “Things have changed since the 1998, 2008, and 2011 downturns,” he says. “It would be dangerous to make an overall or categorywide judgment.”

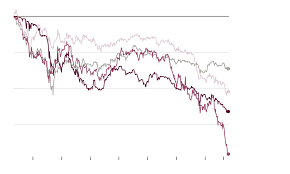

The dean of Franklin Templeton is not alone in seeing longer-term shifts behind the latest debacle of his beloved asset class. Emerging-market equities have crashed by 20% over the past year after treading water for two years, as measured by the widely held iShares MSCI Emerging Markets exchange-traded fund (ticker: EEM). The raw growth that cleansed all sins in times past has tapered significantly. Average economic expansion for developing countries has fallen below 5% annually, from 8% in 2007. Their growth advantage over developed economies is at its lowest since 2002—about 2.5 percentage points.

All of that looks like the new normal, says Rashique Rahman, head of emerging-markets fixed income at Invesco. “We’re looking for a long, drawn-out period of subdued economic growth. It will feel like there’s no end in sight,” he says.

Emerging markets are in part victims of their success. China’s gross domestic product has more than quadrupled since 2001, when Goldman Sachs’ Jim O’Neill coined the phrase BRICs for Brazil, Russia, India, and China. That makes a growth slowdown a mathematical certainty. But the developing world is also “living through the impact of global rebalancing,” says Jorge Mariscal, chief investment officer for emerging markets at UBS Wealth Management.

IN THE GOLDEN AGE of emerging markets, before 2008, rich countries borrowed at a hectic pace, partly to gorge on poorer countries’ goods and commodities. In the silver age—2009 to 2011—deleveraging Western consumers were replaced by a hyperleveraging China, and by global investors eager to lend to faraway companies rather than accept near-zero interest at home. Bond issuance by emerging-market corporates has more than doubled since 2009, to $2.4 trillion.

Those powerful props have fallen away over the past year or two. China tightened its stimulus tap, and growth is slumping there, from 7.8% in 2013 to an expected 6.8% this year and 6% in 2017, according to the International Monetary Fund. China’s arrested development is visible in dozens of so-called ghost cities that were thrown up during the frenetic boom years and now await inhabitants.

China’s slowdown, combined with subpar recovery in the U.S. and Europe, has slashed demand for the wares of other developing countries. Emerging-market exports have stopped growing after posting 10% to 20% annual gains throughout the 2000s, Mariscal says. The Federal Reserve meanwhile ended its quantitative-easing program and signaled, again and again, that it will raise rates eventually.

Funds rushed back to the U.S., emerging markets’ currencies crashed, and their new mountain of debt began to look much more ominous. A Bank for International Settlements report earlier this month found that a half-dozen big markets—led by China itself, Brazil, and Turkey—have ratios of credit to GDP that historically have been associated with “serious banking strains.”

Emerging-market governments and companies did little to prepare for leaner times. National leaders stopped trying to privatize the massive state-owned banks, utilities, and resource producers that clog the heart of many developing economies. Private corporations grew complacent on easy credit. Average return on equity and capital has declined for the past four years straight, says Chuck Knudsen, an emerging-markets equity strategist at T. Rowe Price.

The resulting drop in profits means emerging-market stocks are not as cheap as you might expect. The average forward price/earnings ratio across the asset class is about 10.6, about the same as it was three years ago. “Equities are not quite yet at capitulation levels,” Mariscal says. “There are still some positions to be sold.”

But emerging markets have also improved in some ways over time, and these improvements make fixed-income investment more interesting than equities after the latest wipeout. Nearly two decades have passed since the last full-blown emerging-market crisis, in 1997-98, marked by a wave of sovereign defaults and currency collapses. Governments have learned fiscal discipline since then, save for a few outliers like Venezuela and Argentina.

Bigger debtors should keep paying their bills through the current slowdown, despite jarring downgrades to junk this year for once-prized issuers like Russia and Brazil. “Our base-case scenario is no sovereign defaults among mainstream countries,” says Invesco’s Rahman. That could create opportunity in funds like the iShares Emerging Market USD Bond ETF (EMB), whose price has fallen 6.5% since April, a dramatic move by bond-market standards.

Another change stabilizing emerging markets on a macro level has been a mass shift from pegged to floating currencies, which act as a shock absorber in tough times. Instead of the abrupt meltdowns that afflicted the Korean won, Thai baht, or Mexican peso in crises of yore, EM currencies have lost altitude gradually since mid-2011, scraping 15-year lows against the dollar.

THAT PAINFUL ADJUSTMENT may bottom out soon because cheaper currencies are doing what they are supposed to, cutting import appetites and shrinking the current account deficits that drove devaluation in the first place. That is particularly true for oil importers, which are also getting a big break on fuel prices. India has shown dramatic improvement, its accounts gap shrinking from 4.8% of GDP in 2013 to 0.2% in the first quarter of this year. Turkey and South Africa, which joined India on Morgan Stanley’s much-publicized Fragile Five list two years ago, are also improving steadily.

Against this background, brave investors might want to take a punt on the Wisdom Tree Emerging Currency Strategy fund (CEW), which has fallen 17% over the past year. An indirect way to bet on firming money is through a local-currency bond fund like the iShares Emerging Markets Local Currency Bond ETF (LEMB), which looks suitably beat up with a 21% decline over the past 12 months. Even the more bullish pros warn against betting the farm, however. “We do see value in EM debt, but when one realizes that value remains to be seen,” says Edwin Gutierrez, head of emerging-market sovereign debt at Aberdeen Asset Management.

EMERGING-MARKET EQUITY diehards say they can isolate pockets of the old explosive growth within the larger lackluster landscape. The Chicago-based William Blair Emerging Markets Small Cap Growth fund (BESIX) has been an anomalous outperformer, rising some 30% over the past three years, though it is down 7% year to date.

Fund co-manager Todd McClone says he’s piling into fertile market niches like Chinese pollution-control and alternative-energy firms, or mortgage lenders and private hospitals in India. T. Rowe Price’s Knudsen points to the global growth potential of sectors like insurance and food retailing, even as the emerging-market raw-materials and manufacturing engines sputter.

But few investors will wager heavily on an eclectic portfolio whose liquidity risk is hard for the layman to gauge. McClone’s fund boasts modest assets of $281 million. The dominant EEM ETF holds $21 billion by comparison. It is weighted toward Chinese state banks and mature industrials like Samsung Electronics (005930.Korea) and Taiwan Semiconductor(TSM), which show little promise of outgrowing the macro backdrop. “The rapid growth of ETFs has increased herd behavior as investors focus on beating or at least following the index,” laments Mobius, whose own Templeton Emerging Markets Small Cap fund (TEMMX) has gained 6% over the past three years.

Emerging markets’ greatest strength going forward may be the weakness of competing investments, with multiyear bull runs in the U.S. and Japanese stock markets looking tapped out and the Fed’s restraint indicating that fixed-income yields will remain low in the developed world. The toxic mixture of low growth, high debt, and lagging reform make emerging-market equities unattractive, anyway. But try EM bond markets first, and be careful.